Decentralized financial systems are priori introduced with the development of Bitcoin in 2009 by Satoshi Nakamoto who is/are mystery inventor first cryptographic, peer-to-peer electronic cash system that solves the double-spending problem in the context of financial transactions. Bitcoin is backed by blockchain technology that intervenes in the peer-to-peer architecture of the electronic cash systems that empowers the online value transmission between peers without a trusted third party or any centralized financial institution. As of the Bitcoin deployment to the web services, decentralized alternatives of financial and governmental institutions are rapidly developed to eliminate theoretical financial trust in centralized powers and produce alternative decentralized financial products.

What is Decentralization, and how does it revolutionize?

Decentralization or decentralization is the process by which the activities of an organization, particularly those regarding planning and decision making, are distributed or delegated away from a central, authoritative location or group [1]. In the context of financial applications and hierarchical decision-making, to eliminate theoretical third parties that compose of the assumptions of trust, secure and centralized, decentralization is a recently emerged technology that empowers the distributed and autonomous decision making across parties or peers. Blockchain is the very first technology that capacitated the distributed and decentralized consensus mechanism across a large number of peers by securing the value transmission in an immutable way. It eliminates the a priori need for centralized authority and empowers decentralization such that all users collectively retain control that is implying that no single person or group has control over the mechanism. By temporal-causal inferencing, the first decentralized value transmission system, namely Bitcoin that is backed by blockchain was deployed after the financial crisis in America in 2008 that led to pushing the world’s banking system towards the edge of collapse. Rising energy prices on global markets, leading to an increase in the rate of global inflation worldwide that betray the geographically distributed socio-financial groups’ trust in existing government-oriented financial systems. As Bitcoin proposed a stateless/government-excluded and non-discriminative value transmission technology to society of socio-financial groups, we argue that these groups were the early adapters to the decentralized system. Then, decentralized finance (DeFi) is constructed and shaped by the geographically distributed socio-financial groups with existential governmental groups by controversing or emerging new decentralized technologies such as

- The development of the token economy and the creation of different collateral and financing options

- The establishment of the Decentralized Exchanges (DeX), Decentralized Applications (DApps), Decentralized Autonomous Organizations (DAO) and much more

- Making foreign trade transactions in a decentralized way, from where many steps from money transfer to document exchange is carried out by manual processes, to blockchain-based platforms, in a fast and transparent way

- Reaching more customers for financing and export, and their transaction volumes grow with Initial Coin Offering (ICO)

- The advent of decentralized digital identity that empowers priority issues by both institutions and regulators

- Credit and insurance processes become simpler and faster (intermediary institutions and information requested institutions disappear/switch to this platform)

- Creation of alternative credit platforms in a decentralized manner

- Creation of purchasing / seller-buyer platforms for mechanism design-oriented decentralized incentivization

The mentioned decentralized alternatives are shaped through interpretive flexibility in years with socio-financial and governmental groups towards the notion of closure. As more than 10 years passed, the early majority came up with some sense of closure in the context of blockchain and DeFi.

Bitcoin & Blockchain Primer

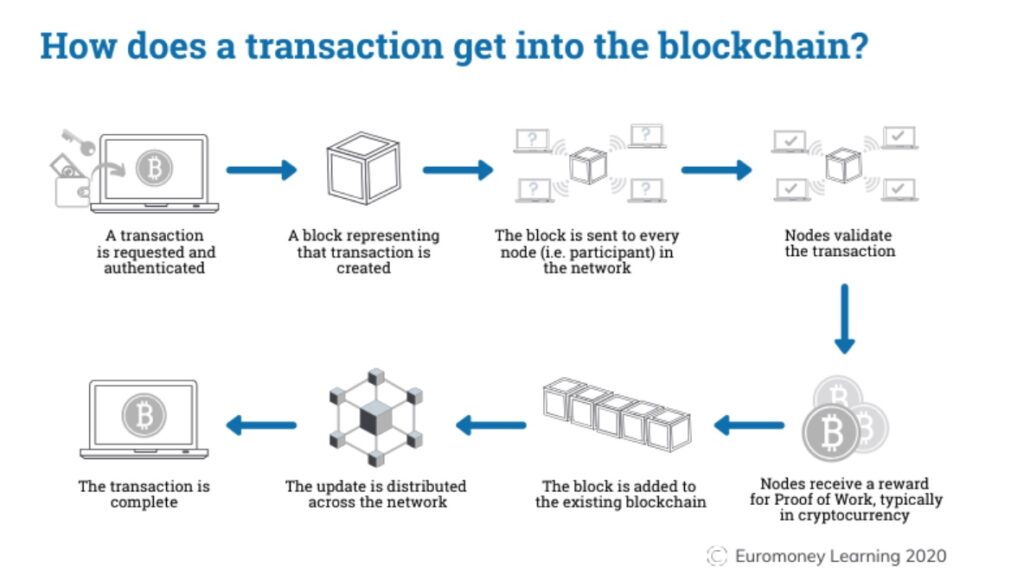

Bitcoin is a decentralized and cryptographically protected electronic currency that is a purely peer-to-peer version of electronic cash that allows online payments to be sent directly from one party to another without going through a financial institution [2]. The network timestamps transactions by hashing them into an ongoing chain of hash-based proof-of-work, forming a record that cannot be changed without redoing the proof-of-work [2]. The longest chain not only serves as proof of the sequence of events witnessed but proof that it came from the largest pool of hash power [2]. Messages and information are broadcast on a best effort basis, and nodes can leave and rejoin the network at will, accepting the longest proof-of-work chain as proof of what happened while they were gone. As Bitcoin is backed by blockchain technology, blockchain is essentially a distributed database of records or public ledger of all transactions or digital events that have been executed and shared among participating parties [3]. Each transaction in the public ledger is verified by the consensus of a majority of the participants in the system [3]. As the on-the-fly information comes from the distributed social agents, and the information is entered into the system, it can never be erased. As a visual representation of how blockchain works, we provide the underlying process and architecture in figure 1.

Conceptually speaking, the lifecycle starts with the social agent that requested a transaction to send a value to the other party. Then, a block representing the transaction is created and broadcasted to every node in the network. As it depends on the consensus mechanism of blockchain, nodes validate the transaction and the transaction is completed. For example, the Proof-of-Work (PoW) based consensus mechanism, introduces a cryptographic and computational puzzle that needs to be solved in order to validate the transaction that requires a computer or hash power. Then, the block is added to the existing blockchain and the transaction is completed. As a reward for validating the transaction, the validator (or miner in PoW) receives a cryptocurrency such as Bitcoin.

Even though Bitcoin itself is still controversial worldwide as a digital currency, blockchain has already found applications from health, energy, law to finance. As the on-the-fly transaction can be recorded in an immutable block of blockchain and distributed across the many nodes in the network of the database, no single entity can corrupt or hack the recorded information that enables decentralized and autonomous decision making. From the socio-ethical perspective, blockchain gives a greater degree of decentralization, empowered by distributed individuals, which enables greater voice, and choice of individual constituents to influence decisions that affect their lives, and of sub-national and local governments to respond dynamically to constituency concerns. Hence, blockchain creates an unalterable record of transactions with end-to-end encryption, which shuts out fraud and unauthorized activity that improves security and privacy.

On the other side, blockchain is visible and traceable. On-the-fly private information is visible to the public, as everyone can see the transaction between entities from the emergence of Bitcoin. Carefully note that the encrypted information is visible in the public ledger, not the pure private information itself that enables pseudo-anonymity. By pseudo-anonymity, it is meant to be that a person will be linked to a public cryptocurrency address, such as Bitcoin and Ethereum, but no one will get to know the actual name or address. As pseudo-anonymity implies, ever-growing transactions in the form of value and information are purely traceable by anyone.

The Real Business: Decentralized Finance (DeFi)

Decentralized finance (DeFi) refers to an alternative financial infrastructure, as opposed to the centralized one, built on top of the smart contract-based blockchains [4]. DeFi uses smart contracts to create protocols that replicate and innovate existing financial services in a more open, interoperable, and transparent way [4]. DeFi creates hope for socio-financial groups by enabling trusted financial products which are built from tamper-proof digital smart contracts interacting with blockchains. Decentralization allows socio-financial groups to be their own bank, which doesn’t necessarily hold money but the values of any kind. As DeFi offers open, permissionless, and censorship-resistant financial protocol that is backed by algorithmic smart contracts, it eliminates the need for intermediaries and centralized financial organizations. It is generally packaged and deployed by decentralized applications (DApps) on protocol layer blockchains such as Ethereum for the exchange of values.

DeFi already offers a wide variety of applications. For example, one can buy U.S. dollar (USD)-pegged assets (so-called stablecoins) on decentralized exchanges, move these assets to an equally decentralized lending platform to earn interest, and subsequently add the interest-bearing instruments to a decentralized liquidity pool or an on-chain investment fund [4].

From the blockchain-oriented business development frameworks, Initial Coin Offerings (ICOs) offer a decentralized way of raising fundings by distributing the tokens to a theoretically large number of users. As generally, the blockchain startups have their own ecosystem, the distributed tokens have economical payoffs or some sense of utility in their products, or it represents the stake in the startup.

As smart contracts are algorithmic laws specified by their developers to run on on-chain decentralized applications, their behavior is fixed and ensures the delivery of the same service to everyone without discriminating. As opposed to the client-server architecture that is highly centralized, its deterministic behavior and decentralized model eliminate the risks of theoretical manipulation by the servers.

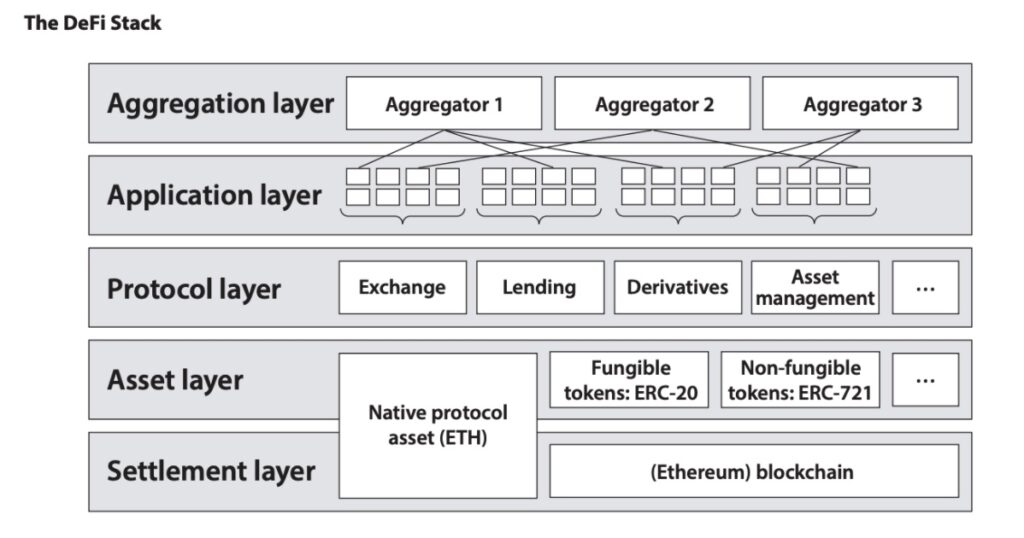

DeFi uses a multi-layered architecture [4]. Every layer has a distinct purpose with building on each other and creating an open and highly composable infrastructure that allows everyone to build on, rehash, or use other parts of the stack like the internet [4]. It is also crucial to understand that these layers are hierarchical, which means they are only as secure as the layers below [4]. The DeFi stack is provided as visual in figure 2.

The stack is drawn for Ethereum based DeFi products. In the settlement layer, value exchange is done in the Ethereum blockchain that theoretically ensures the security, pseudo-anonymity, and scalability of the system. In the settlement layer, public blockchain and distributed ledger exist. Then, the value swap protocols are developed in the asset layer to specify the product requirements. On top of the asset layer, the protocol layer is embedded to specify the product type and its protocols, such as lending, borrowing, derivatives, and so on. In parallel with real-world institutions, this would be a set of principles and rules that all participants in a given industry have agreed to follow as a prerequisite to operating in the industry [10]. Then, the applications layer is where consumer-facing applications reside and abstract underlying protocols into simple consumer-focused services [10]. As the last layer, the aggregation layer consists of aggregators who connect various applications from the previous layer to provide a service to investors [10].

Lastly, the reader should keep in mind that centralized financial systems are usually very heavily regulated as opposed to decentralized alternatives, the reason that the decentralized alternatives are not much regulated is due to economical and political standpoints, as they pose inherent technological, conceptual, and contextual challenges to regulatory systems.

Author: Can Kocagil

References

- Wikipedia contributors. “Decentralization.” Wikipedia, The Free Encyclopedia. Wikipedia, The Free Encyclopedia, 18 Oct. 2021. Web. 19 Oct. 2021.

- Nakamoto, Satoshi. (2009). Bitcoin: A Peer-to-Peer Electronic Cash System. Cryptography Mailing list at https://metzdowd.com.

- Blockchain technology — home — UC Berkeley sutardja center. (n.d.). Retrieved October 21, 2021, from https://scet.berkeley.edu/wp-content/uploads/BlockchainPaper.pdf.

- Schär, Fabian, Decentralized Finance: On Blockchain- and Smart Contract-Based Financial Markets (April 2021). Available at SSRN: https://ssrn.com/abstract=3843844 or http://dx.doi.org/10.20955/r.103.153-74

- “The Social And Political Costs Of The Financial Crisis, 10 Years Later”. Harvard Business Review, 2021, https://hbr.org/2018/09/the-social-and-political-costs-of-the-financial-crisis-10-years-later.

- United Nations. (n.d.). The social impact of the economic crisis | DISD. United Nations. Retrieved October 21, 2021, from https://www.un.org/development/desa/dspd/world-social-report/2011-2/the-social-impact-of-the-economic-crisis.html.

- Klein, Hans K., and Daniel Lee Kleinman. “The Social Construction of Technology: Structural Considerations.” Science, Technology, & Human Values, vol. 27, no. 1, Jan. 2002, pp. 28–52, doi:10.1177/016224390202700102.

- Bijker, W. E. (2001). Technology, social construction of. International Encyclopedia of the Social & Behavioral Sciences, 15522–15527. https://doi.org/10.1016/b0-08-043076-7/03169-7

- Wikipedia contributors. “Social construction of technology.” Wikipedia, The Free Encyclopedia. Wikipedia, The Free Encyclopedia, 24 Apr. 2021. Web. 21 Oct. 2021.

- Sharma, R. (2021, August 19). Decentralized finance (DEFI) definition and use cases. Investopedia. Retrieved October 21, 2021, from https://www.investopedia.com/decentralized-finance-defi-5113835.

Cover Image: Image by Zoltan Tasi in Unsplash